{kind=link}

Submitted by Wilfred Rhaburn, CPA, Managing Partner, W. Rhaburn Consulting

The Belize Income Tax Department is currently holding country wide consultations on the contract tax and the withholding tax on payment to non residents for technical and management services (the “withholding tax”) as provided for in the Income and Business Tax Act. On February 24, 2014, the Income Tax Department made a presentation on the contract tax and withholding tax in San Pedro at the Lion’s Den.

The Belize Income Tax Department is currently holding country wide consultations on the contract tax and the withholding tax on payment to non residents for technical and management services (the “withholding tax”) as provided for in the Income and Business Tax Act. On February 24, 2014, the Income Tax Department made a presentation on the contract tax and withholding tax in San Pedro at the Lion’s Den.

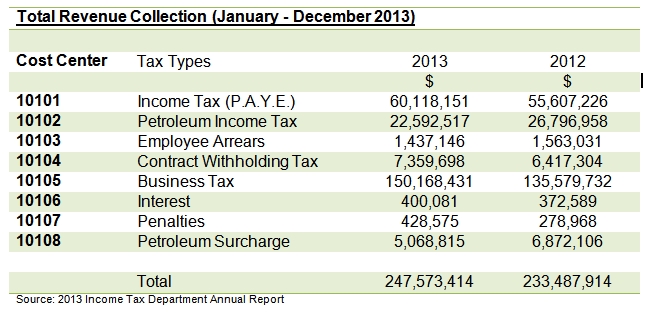

The contract tax and withholding tax on payments to non residents are not new taxes but have been in existence since 1998 (when the business tax was implemented). In 2013, the Income Tax Department collected $7,359,698 in contract tax withholding ($6,417,304 in 2012). With renewed tax payer education and awareness, the Income Tax Department is hoping to improve the compliance rate of the contract tax and withholding tax (non residents) and by extension increase revenue collections.

Below is a table of total revenue collections by the Income Tax Department for 2013.

Contract Tax Withholding

Contract Tax Withholding

Section 112 of the Belize Income and Business Tax Act states that for all contracts in excess of $3,000 annually a withholding of 3% must be made from all gross contract payments, without deductions. The payer has an obligation to withhold and remit the contract tax withheld and can be held liable for the tax if they fail to do so. Also, the service provider must provide to the payer, their Income Tax Department tax identification number (TIN) or if they do not have a TIN, some other form of Identification including social security number.

The contract tax withheld must be paid over to the Government of Belize, Income Tax Department by the 15th of every month for the previous month, using Form TD 25, “Gross Contract Payments, Remittance of Tax Withheld From Contract Payments.” The contract tax withheld acts as a credit towards the monthly business tax payable by the supplier.

Furthermore, as per Section 112 of the Income and Business Tax Act, a contract means a contract awarded to or to be performed by a self- employed person, professional or entity for the carrying out of works or services, or for the supply of labor or materials. As such, the contract tax withholding applies to accounting, legal, management services, plumbing, electrical, construction, brokerage, transportation, rent and other service providers. Payments made for outright sale of products, utilities, insurance premiums, to banks and financial institutions, Government of Belize, Statutory Bodies, Local Authorities are exempt from the contract tax withholding. In addition, contracts for the sale of real estate, royalties and commissions, payments for general sales and accommodation taxes are also exempt. The contract tax provision does not apply to export processing zone businesses (EPZ), representatives of foreign countries and those having diplomatic status. In cases where the supplier’s business tax rate is lower than the 3% withholding, the Commissioner of Income Tax after receiving a written request, may reduce and certify the withholding rate to lower than 3% withholding. The Commissioner of Income Tax can also increase the withholding tax rate if he deems it necessary.

Furthermore, as per Section 112 of the Income and Business Tax Act, a contract means a contract awarded to or to be performed by a self- employed person, professional or entity for the carrying out of works or services, or for the supply of labor or materials. As such, the contract tax withholding applies to accounting, legal, management services, plumbing, electrical, construction, brokerage, transportation, rent and other service providers. Payments made for outright sale of products, utilities, insurance premiums, to banks and financial institutions, Government of Belize, Statutory Bodies, Local Authorities are exempt from the contract tax withholding. In addition, contracts for the sale of real estate, royalties and commissions, payments for general sales and accommodation taxes are also exempt. The contract tax provision does not apply to export processing zone businesses (EPZ), representatives of foreign countries and those having diplomatic status. In cases where the supplier’s business tax rate is lower than the 3% withholding, the Commissioner of Income Tax after receiving a written request, may reduce and certify the withholding rate to lower than 3% withholding. The Commissioner of Income Tax can also increase the withholding tax rate if he deems it necessary.

Withholding Tax from Remittances to Non Residents

The Income Tax Department is also enforcing Section 113 (3) and (4) of the Income and Business Tax Act. Section 113 (3) and (4) places a 25% withholding tax on payments to a non resident for management fees, professional or technical fees and insurance premiums. There is also a 15% withholding on interest on loans paid to non residents. The above mentioned withholdings are assessed only on the service element of the payment. Furthermore, there are additional provisions for special treatment of payments made to recipient resident in “Treaty Countries.”

Note that a person is considered a Belize resident for tax purposes if they spent in the aggregate more than one hundred and eighty-two days within the country in that basis year or was domiciled in Belize.

The withholding tax on payments to non residents must be paid over to the Government of Belize, Income Tax Department by the 15th of every month for the previous month, using Form TD 29, “Withholding Tax Payments.”

The Income Tax Department Auditors will be performing compliance audits on the contract tax and withholding tax on payments non residents commencing in April 2014 and business persons/entities are advised to modify their accounting system and software to better account for contract tax and withholding tax payments to non residents.

Wilfred Rhaburn may be contacted for assistance on the contract tax and withholding tax on payments to non residents and related compliance issues. Rhaburn, CPA, is Managing Partner at W. Rhaburn Consulting, located at Vilma Linda Plaza in downtown San Pedro, AC. He may be reached at 610-4407 or at wrhaburn@consultingbelize.com.